Retirement Watch is a financial newsletter led by Bob Carlson.

As part of a 2023 promotion, all new subscriptions to Retirement Watch come with a free copy of The New American Retirement Plan and a bundle of other bonuses to protect your retirement savings.

Keep reading to find out everything you need to know about Retirement Watch and The New American Retirement Plan today in our review.

What is Retirement Watch?

Bob Carlson’s Retirement Watch is a monthly subscription service featuring stock recommendations, investment ideas, and market analysis.

The subscription is marketed mostly to retirees and those approaching retirement age. Bob Carlson also discusses concepts like taxes in retirement, individual retirement accounts (IRAs), estate planning, and more.

Bob Carlson and his team have launched a new promotion for Retirement Watch in 2023. All new subscriptions to Retirement Watch come with a bundle of bonus reports and guides. The goal of this package is to help investors protect their retirement savings from future market turmoil.

Bob is warning retirees of the impacts of a new law. That law will devastate the 401(k)s, IRAs, and Roth IRAs for investors across the United States. The law upends 20 years of retirement planning and devastates the savings of the middle class.

By subscribing to Retirement Watch today, you can discover how to avoid the ramifications of this new law and protect your retirement money.

Why is Congress Coming for Your Retirement Savings?

Bob Carlson claims Congress is coming for the retirement savings of middle-class Americans with a new law.

That new law is set to devastate your 401(k)s, IRAs, and Roth IRAs while destroying 20 years of retirement planning.

Here’s how Bob explains it:

“…the U.S. government just enacted the most devastating law I’ve seen in my 30-plus years as a retirement expert. This new law is set to significantly reduce the value of your 401(k)s… your IRAs… (yes, even your Roth IRAs)… and even your pension, if you have one of those.”

All of the money you’ve saved away for your entire life will be taken away by Congress, according to Bob.

The best way to save your retirement is to subscribe to Retirement Watch today and receive a free copy of The New American Retirement Plan. In the book, Bob recommends new strategies to follow to safeguard and grow your retirement accounts over the coming years – before the government takes your savings away.

What is The New American Retirement Plan?

All new subscriptions to Retirement Watch come with a free bonus book called The New American Retirement Plan.

Bob describes the book as a “retirement survival guide.” It helps investors of all ages navigate the government’s new retirement account rules.

By following the strategies in this guide, you could protect and grow your savings while insulating your savings from Congress’s decisions.

Just read the book, follow the recommended steps, and save your retirement.

Bob explains the specific steps to take today to protect your retirement accounts, including the very first move to make to avoid having the government steal your IRAs and 401(k). Bob introduces a total of seven “end-around maneuvers” to prevent the government from taking your retirement money.

How is Congress Taking Your Money?

According to Bob Carlson, the United States Congress has voted to take retirement account money away from ordinary, middle-class Americans.

The House recently passed the bill by an overwhelming margin, with only 3 of 420 elected representatives voting no (and 15 reps not showing up).

The bill didn’t generate much attention from the media. It stalled for a while, then breezed through the Senate before being signed into law by the President.

Because of the bill, according to Bob, millions of Americans are about to lose their retirement savings:

“…the retirements of so many Americans…are about to go up in smoke.”

So why is Congress taking away your retirement savings? What will happen to ordinary investors with retirement accounts?

As an example, Bob mentions the average 62-year old. That person has saved his entire life and done everything possible to ensure a comfortable retirement. That person also wants to extend retirement savings to loved ones after passing on. Because of the passing of this law, this ordinary investor will have significantly less money in a 401(k), traditional IRA, and Roth IRA. That person will also have less money to pass to children and grandchildren after passing:

“…it doesn’t even matter how much or how little you have. If your money’s in a 401(k)… they’re coming for it. If it’s in a traditional IRA or a Roth IRA… they’re coming for it. Heck, if it’s in your kids’ or grandchildren’s college funds… they’ll come for that, too.”

In fact, Bob claims Congress isn’t stopping there. The bill is just the first step of a plot to ruin the retirements of millions of Americans:

“…that’s just the first in a series of nefarious plots they’re planning.”

By following Bob’s advice today, however, investors can protect their retirement accounts from Congress, avoid the ramifications of this new law, and secure their legacy.

Why is Congress Taking Retirement Savings?

We know how Congress plans to take away Americans’ retirement accounts. However, we don’t know why Congress is planning to do it.

Bob believes Congress is facing a crisis:

America has roughly 75 million baby boomers. Roughly 25% of the country’s population are baby boomers.

Over the last few decades, many baby boomers have contributed enormous amounts to their Roth IRAs, traditional IRAs, and 401(k)s. There’s now trillions of dollars tied into these investment vehicles.

As baby boomers are starting to retire, they’re cracking open these retirement nest eggs to pay for college tuition, weddings, and retirement expenses.

Unfortunately, Congress is facing a crisis: Social Security is expected to run out in 2034. Medicare is also getting more expensive every year. As baby boomers get older, these problems are expected to get worse.

To fight this issue, Congress plans to change the withdrawal requirements for IRAs. They also plan to increase taxes on all retirement accounts and IRAs.

Fortunately, by making changes to your retirement accounts today, as Bob Carlson recommends, you can avoid losing the full value of your retirement accounts.

What Will You Learn in The New American Retirement Plan?

Bob Carlson has written an all-in-one text explaining how to protect your retirement savings. It’s called The New American Retirement Plan.

The book features four separate sections, and each section is packed with hundreds of tips, strategies, loopholes, and guides to help you navigate your retirement.

By subscribing to Retirement Watch today, you get complete access to the book and all of the investment advice included inside.

Here are some of the topics covered in the book:

The same blueprint Bob Carlson is using for his own retirement in a highly specific and highly personal way. Bob has been a retirement specialist for 30 years, and he knows retirement savings strategies better than virtually anyone.

Why, according to Social Security whistleblowers and other insiders, many retirees will not receive as much as they think from Social Security.

How individuals and married couples can make one simple move to put an extra $25,000 or more in their pockets (page 129).

How to maximize your Social Security benefits and get up to 76% more on your monthly payouts (page 43).

How to legally offset the spiraling costs of long-term care (LTC) medical expenses, potentially saving you tens of thousands of dollars (page 182).

How to create a monthly, tax-free income stream to last the rest of your life (page 77).

How to avoid the worst impacts of Congress’s new retirement account distribution laws and tax penalties to keep as much of your retirement savings as possible.

Why the traditional 4% annual retirement withdrawal rate is often completely wrong for people today – and what you should do instead to ensure a safe and happy retirement (page 55).

How to use an “end-around” maneuver to avoid Congress’s new retirement law.

7 specific strategies you can use to accomplish the “end-around” maneuver, ranging from simple strategies to more complicated options. Bob lays out the strategies, letting you choose which one is best for your situation (page 62).

How to protect yourself from the retiree tax attack, including why your taxes are likely to increase during retirement after changes introduced in the 2017 tax law (page 24).

Why Medicare and your employer’s insurance is unlikely to cover most retirement medical expenses and long-term care costs, and why medical expenses will be one of the three biggest retirement expenses for most retirees.

How to guarantee you never outlive your money in retirement (page 9).

How to get 76% more on your Social Security payouts (page 136).

How to take advantage of a little-known method to add up to $37,000 to a tax-free retirement account every year. The strategy is completely legal and above board, and it may be particularly important because of Congress’s new changes.

Detailed tips from the estate plans of major celebrities who successfully navigated complicated retirement and inheritance situations, using proven strategies to maximize retirement savings. The book highlights stories from Prince, Tom Petty, Aretha Franklin, Stan Lee, and other high net worth individuals who successfully navigated a complicated retirement situation.

How to get paid monthly or quarterly using Bob’s recommended retirement paycheck portfolio (page 35).

How to collect tax-free payouts, every month for life (page 68).

3 changes every American should consider for their estate plan – no matter how much money you have (page 143).

Mutual fund tax secrets 99% of Americans are unaware of – but that could save you a lot of money on taxes (page 97).

The best practices for IRA investing, including do’s and don’ts to survive Congress’s new law (page 72).

The legal loophole you can use to reduce medical costs (page 103).

The retirement calendar checklist, including a simple strategy to ensure your retirement affairs are in order (page 10).

Overall, Bob sees The New American Retirement Plan as the result of his personal mission to create a brand-new approach to retirement. He started to research the plan as soon as he heard about Congress’s new changes. Now, he’s encouraging all Americans concerned about retirement to follow the guide to secure their savings.

What’s Included with Retirement Watch?

If you subscribe to Retirement Watch today, you get instant access to The New American Retirement Plan, as highlighted above. However, you also get access to a bundle of additional bonus reports covering retirement and more.

Here are all of the bonus reports and guides you receive when you subscribe to Retirement Watch today:

12 Month Subscription to Retirement Watch: Each month, Bob sends a new issue of his newsletter to subscribers. Bob has sent a new monthly issue of Retirement Watch every month since 1991. Each issue is packed with expert answers and simple solutions to help you avoid running out of money in retirement. It’s a powerful retirement planning tool to help eliminate worry and guesswork while maximizing every dollar in your retirement accounts.

Free Copy of The New American Retirement Plan: All new subscriptions to Retirement Watch come with a free copy of The New American Retirement Plan. The 190-page book features tips for maximizing retirement finances, strategies for avoiding Congress’s new retirement account laws, and other tips for holding onto your retirement savings. Bob tells you, in specific and personal detail, how he is managing his own finances in response to Congress’s new retirement and savings laws.

Access to Retirement Watch’s 5 Easy Chair Proprietary Investment Portfolios: Bob Carlson publishes five “easy chair” proprietary investment portfolios through Retirement Watch. Subscribers can view the holdings in each portfolio, their past returns and predicted gains, and their level of risk. You can choose one of the five retirement plans that works for your unique needs.

Members-Only Live Conference Calls: Bob Carlson hosts live conference calls where subscribers can ask questions directly. During conference calls, Bob also updates subscribers on the most pressing retirement issues of the day, changes to the five model portfolios, and any other notable news or adjustments.

Immediate Access to Members-Only Retirement Watch Website: Subscribers receive complete access to the Retirement Watch website. The members-only website makes it easy to access the most recent newsletter issue, additional free special reports from Bob, past issues and reports, and all other membership perks.

Access to Full-time Customer Service Staff: Subscribers receive complete access to the Retirement Watch customer service team, which works full-time to answer questions, adjust subscriptions, and handle requests.

Online Retirement Spending Calculator: The #1 fear most retirees have is running out of money in retirement. Subscribers receive access to an online retirement spending calculator. This calculator checks your expenses, adds in other hidden costs of retirement, mixes in the effects of inflation, and determines how much you can safely spend to avoid running out of money.

Ongoing Retirement Education Series: Bob regularly educates subscribers with a series of reports, helping subscribers become smarter about their retirement while making more profitable decisions about their future and their money.

Free Access to Retirement Watch Conferences Across the United States: All Retirement Watch subscribers receive free access to Bob Carlson’s retirement conferences taking place across the United States. Recent events have taken place in Philadelphia, Orlando, Las Vegas, San Francisco, and other cities.

Bonus Report #1: Cashing in Congress’ $350,000 “Retirement Shocker”: This is the first volume in Bob Carlson’s Ultimate Retirement Library. It explains the impacts of new major changes from Congress letting you add an additional $350,000 to your retirement. You can see how these changes work, how they’ll impact your retirement, and how to avoid the worst implications of these strategies. The book is valued at $179 and included for free with new subscriptions to Retirement Watch.

Bonus Report #2: The New Rules of Retirement: This special report was recently updated to address the new changes in Congress. Bob sees this report as “the cornerstone” of his work because it helps retirees and pre-retirees solve the two biggest, most overlooked threats to their retirement. In the report, you can discover how to manage the time bomb in your IRA that starts ticking the moment you retire. You can also discover how to protect your lifetime income stream. By identifying these threats early, you can protect your retirement. The report is valued at $129 and available for free with new subscriptions.

Bonus Report #3: Gimme Shelter: Hidden Real Estate Time Bombs to Avoid: This report is the third report in the Ultimate Retirement Library. For many retirees, their home is their most valuable asset. Unfortunately, taxes and penalties could inhibit the value of this asset, leaving many retirees with a surprising tax bomb. This report explains how to navigate this issue to protect your retirement.

Bonus Report #4: Your 20-Minute Estate Plan: Building a Lasting Legacy: This report features a comprehensive, easy-to-understand guide on helping your heirs avoid needless taxes on an inherited IRA, helping your legacy live on. Many retirees are surprised by how many taxes they could pay when passing an IRA to loved ones. This guide explains how to protect your legacy within a 20-minute, easy-to-implement system.

Bonus Guide #5: The Truth About Annuities — And How to Make Them a Lifetime Stream of Income: Annuities are not all created equal. In this report, Bob explores the truth about annuities in a no-nonsense way. Retirees can decide which type of annuity is best for their unique situation – if any. This is the fifth and final volume in the Ultimate Retirement Library, and it’s valued at $49.

Bonus Guide #6: The IRA Investment Guide: A Roadmap to Avoiding Tax Traps & Penalties: Individual retirement accounts are a great way to save for retirement. Unfortunately, it’s also easy to fall into tax traps and penalties that significantly lower the value of your accounts. In this guide, Bob uses his 30+ years of retirement planning experience to explain how to maximize the value of your IRAs.

Bonus Guide #7: How to Insure Your Way to a Rock-Solid Retirement: Insurance is important in retirement. Some retirees are over-insured, spending too much for too little protection. Others are under-insured, leaving them exposed to significant risk.

Bonus Guide #8: Keep Your Nest Egg Safe from the IRS Money Grab: The IRS doesn’t stop chasing you in retirement. In fact, many retirees pay costly IRS penalties every year. In this bonus guide, you can discover proven strategies for keeping your nest egg safe from the IRS.

Bonus Guide #9: How to Inflation-Proof Your Nest Eggs with ETFs: In addition to worrying about taxes and penalties, retirees need to worry about inflation. The money you have in your account today will not be worth as much ten years from now because of inflation. In this guide, you can discover how to protect your nest egg from inflation using the power of ETFs.

100% No-Risk Moneyback Guarantee: All purchases come with a 30 day moneyback guarantee. you can request a complete refund within 30 days. Plus, you can keep all bonus subscriptions as a thanks for trying the membership.

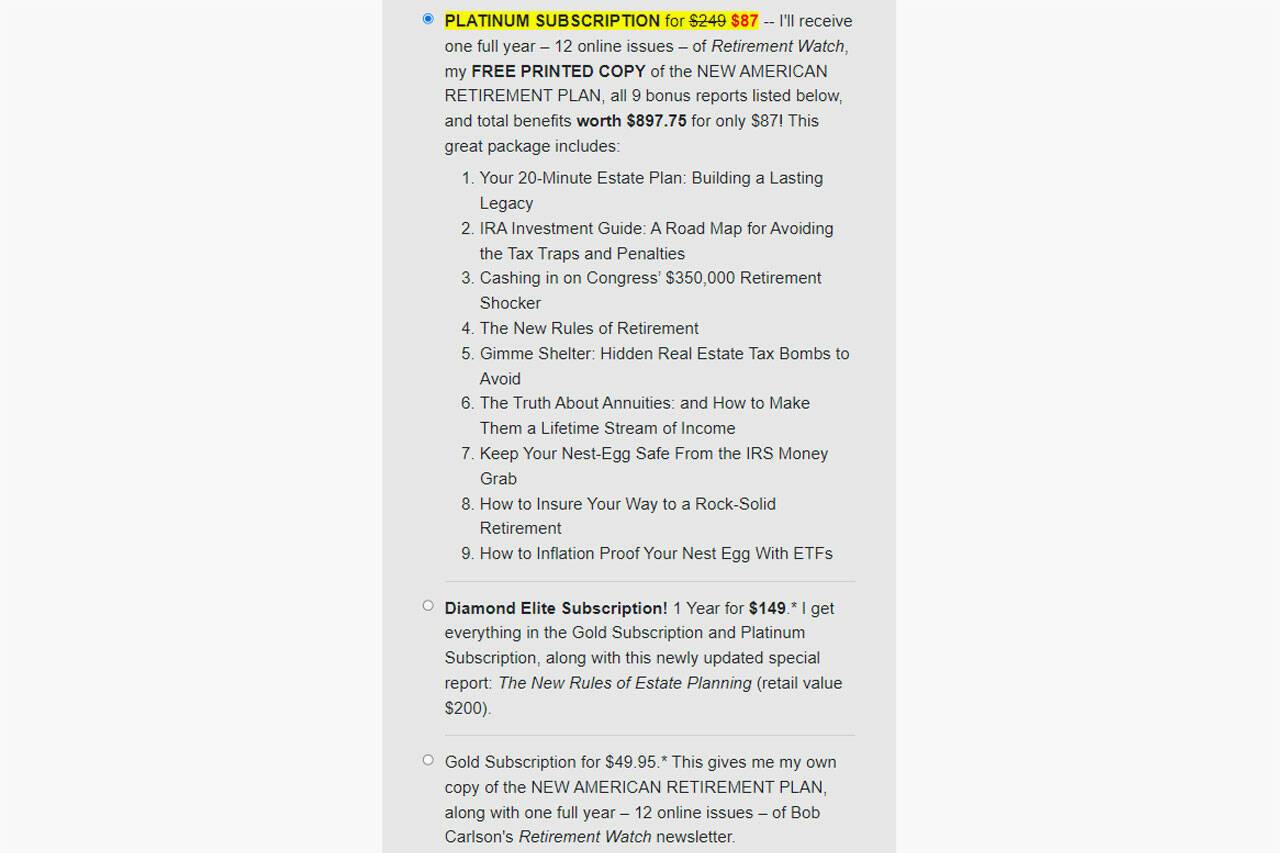

Retirement Watch Pricing

Retirement Watch is normally priced at $249 per year. As part of a 2023 promotion, Bob and his team have reduced the price as low as $49 to $149 per year.

There are three Retirement Watch subscription tiers, including:

Gold Subscription ($49.95)

- 12 online issues of Bob Carlson’s Retirement Watch newsletter

- 1 free digital copy of The New American Retirement Plan

Platinum Subscription ($87)

- 12 online issues of Retirement Watch

- 1 free printed copy of The New American Retirement Plan

- All 9 bonus reports

Diamond Subscription ($149)

- Everything included in the Gold and Platinum subscriptions

- Bonus guide The New Rules of Estate Planning

- All subscriptions automatically renew at the end of your renewal period. You can cancel your subscription at any time.

Retirement Watch Refund Policy

Retirement Watch is backed by a 30 day moneyback guarantee.

You have a full month to decide if Retirement Watch is the right choice for you. If you’re unhappy for any reason, then you can receive a complete refund on your membership fee.

Who is Bob Carlson?

Bob Carlson has a background in accounting and law. He has a law degree and a Master’s degree in accounting from the University of Virginia. He also passed his CPA exam on his very first try.

After deciding he wasn’t destined for the courtroom, Bob took a different approach: he decided to use his knowledge to carve out a badly-needed niche.

Bob created a service to help retirees and pre-retirees help themselves. Over the past 30 years, Bob has grown a reputation as one of America’s experts on retirement.

Launched in 1991, Retirement Watch has helped retirees and pre-retirees for over 30 years. Bob has published a new issue of the newsletter every month.

Bob is also a senior contributor to Forbes.com and an author of three popular books (The New Rules of Retirement, Personal Finance After 50 for Dummies, and Invest Like a Fox… Not Like a Hedgehog).

About The Center for Retirement Security

The Center for Retirement Security is a financial publishing company led by Bob Carlson. Bob Carlson founded the institution in 1989 as a research and collaboration vehicle for retirement and investing.

You can contact The Center for Retirement Security and the Retirement Watch customer service team via the following:

- Phone: 800-552-1152

- Email: customerservice@retirementwatch.com

- Mailing Address: PO Box 1901 Williamsport, PA 17701-1901

Final Word

Retirement Watch is a monthly investment advisory designed for anyone concerned about retirement and their investment accounts.

By subscribing to Retirement Watch today, you receive a free copy of The New American Retirement Plan. In the book, Bob Carlson explains how to navigate Congress’s new retirement laws to ensure you have the retirement you deserve.

All new subscriptions also come with a bundle of 9 bonus reports covering other areas of retirement.

Overall, Retirement Watch and the bundle of bonus reports are seen as retired reading for anyone over 50 – or anyone concerned about their retirement.

ALSO READ: